Lemonade Stock Price Today: Why LMND Is Up Big After Q3 2025 Earnings

Lemonade, Inc. (NYSE: LMND), the AI-powered insurtech company disrupting the traditional insurance market, saw its stock price skyrocket following the release of its third-quarter 2025 earnings. The company, known for its fully digital platform offering renters, homeowners, pet, life, and car insurance, delivered results that significantly exceeded market expectations — igniting investor enthusiasm. LMND shares surged over 30% in a single day, marking one of the most substantial rallies in its recent trading history.

Q3 2025 Earnings Overview

Lemonade’s third-quarter 2025 results marked a pivotal moment in its growth trajectory. The company reported $194.5 million in revenue, representing a 42% year-over-year increase, and surpassing analyst expectations of approximately $185 million. This robust top-line growth was fueled by continued expansion across all insurance lines and improved pricing strategies supported by the company’s AI underwriting.

The company’s in-force premium (IFP) — a key growth metric — reached $1.16 billion, up 30% from the previous year. Notably, this marked the eighth consecutive quarter of accelerating IFP growth. Customer count grew to 2.87 million, a 24% YoY rise, further reinforcing Lemonade’s traction in a traditionally rigid industry.

Profitability metrics also showed improvement. The loss ratio declined to 62%, down from 73% earlier this year — the lowest in the company’s history. Meanwhile, net losses narrowed significantly to $37.5 million, or –$0.51 per share, beating the consensus estimate of –$0.70. Adjusted EBITDA came in at –$26 million, a 50% improvement year-over-year.

A major milestone: Lemonade posted positive cash flow, generating $18 million in adjusted free cash flow and $5 million in operating cash flow — the first time it’s done so in a quarterly report.

Co-founder and President Shai Wininger described the quarter as “the strongest in the company’s history,” citing both financial and operational execution. The company also raised its full-year revenue guidance, projecting $727–732 million for FY2025, up from prior guidance of $710–716 million.

Stock Price Reaction and Recent Movement

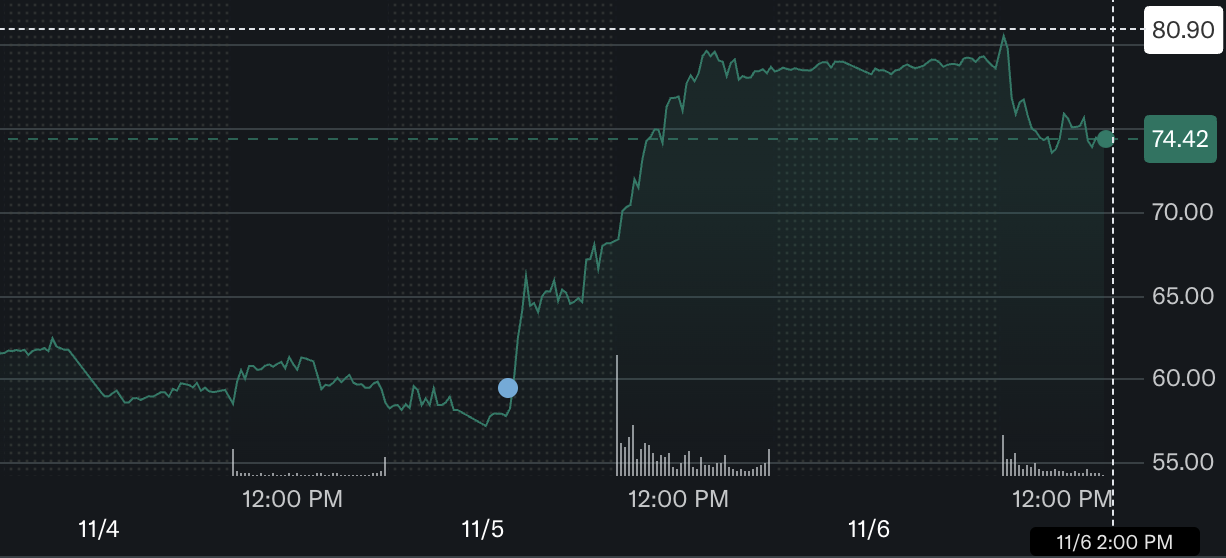

Lemonade, Inc. (NYSE: LMND) Price

Source: Yahoo Finance

Lemonade’s stellar Q3 2025 earnings triggered an immediate and dramatic rally in its stock price. Shares of LMND surged over 30% the day following the earnings release, climbing from around $58 to $76 and notching one of the stock’s most explosive single-day moves since its IPO. Trading volume spiked to over 7 million shares, nearly triple the daily average, signaling widespread investor interest.

The stock continued to show strong momentum into early November, briefly touching an intraday high of $81.90 before settling in the $73–$75 range. As of the latest close on November 6, 2025, Lemonade was trading at approximately $73.55, with a market capitalization hovering around $5.5 billion.

One factor contributing to the sharp price movement was likely a short squeeze. With roughly 25% of Lemonade’s public float previously sold short, the better-than-expected financials may have forced bearish traders to rapidly cover positions, further amplifying the upward momentum.

The rally reflects a clear market re-rating of Lemonade’s near-term potential. Investors are increasingly viewing the company not just as a high-growth disruptor, but as one that’s beginning to demonstrate operational discipline and a credible path toward profitability.

Wall Street Cautious, Retail Investors Bullish: The Sentiment Split on LMND

While investors have enthusiastically rewarded Lemonade’s Q3 performance, Wall Street analysts remain more cautious. The stock has significantly outperformed the broader market in 2025, rallying over 60% year-to-date compared to the S&P 500’s ~15% gain. Despite this momentum, LMND continues to carry a “Hold” to “Moderate Sell” consensus rating among analysts, reflecting lingering skepticism about the company’s path to sustainable profitability.

The average 12-month analyst price target currently sits near $44, implying a substantial downside from its current price in the mid-$70s. This valuation gap highlights concerns about the stock’s premium multiples — particularly its high price-to-sales ratio, which now exceeds 10x trailing revenue. For many analysts, Lemonade’s strong growth and improving loss ratios aren’t yet enough to justify its elevated valuation.

That said, sentiment is beginning to shift. Some firms have acknowledged the company’s operational improvements and raised their targets slightly in response to Q3’s beat. On the retail side, sentiment has been more bullish. Call option volume surged after earnings, and Lemonade remains a popular name on social platforms, with investors highlighting the company’s improving fundamentals and AI-driven operating model. The market’s tone is split: cautious optimism among professionals, and more enthusiastic buying pressure from retail investors and momentum-driven traders.

Price Prediction and Future Outlook

Lemonade’s Q3 results have reset expectations — both for its near-term financials and its long-term stock trajectory. Management has raised its full-year 2025 revenue guidance to between $727 million and $732 million, up from a prior range of $710–716 million. It also narrowed its projected adjusted EBITDA loss to $127–130 million, signaling stronger cost control and operating leverage.

Looking ahead to Q4 2025, Lemonade expects revenue between $217 million and $222 million, slightly above analysts’ consensus. The company continues to target positive adjusted EBITDA by Q4 2026, which would mark a major milestone in its evolution from a fast-growing disruptor to a sustainable business.

In terms of stock price direction, predictions are mixed. From a fundamental standpoint, if Lemonade maintains 30%+ annual in-force premium growth while improving its loss ratio and cash flow, it could justify its current valuation — or even exceed it. In that case, analysts may be forced to revise their $40–$50 price targets upward.

However, any misstep — slower growth, worsening loss trends, or macroeconomic headwinds — could lead to a sharp correction, especially given the stock’s elevated price-to-sales multiple and recent volatility. High short interest could also re-emerge if optimism fades.

Conclusion

Lemonade’s Q3 2025 results have positioned the company at a critical turning point. With accelerating revenue growth, improving loss ratios, and its first quarter of positive cash flow, the insurtech has begun to back its bold vision with tangible financial progress. Investors responded swiftly, pushing LMND shares up over 30% and signaling renewed confidence in the company’s long-term potential.

However, the road ahead still requires careful execution. While management has raised guidance and reiterated its goal of reaching adjusted EBITDA profitability by late 2026, analysts remain cautious, pointing to high valuation multiples and an unproven track record of sustained earnings. If Lemonade can deliver consistent performance over the next few quarters, it may continue to reward shareholders — but expectations are now higher than ever.

Disclaimer: The opinions expressed in this article are for informational purposes only. This article does not constitute an endorsement of any of the products and services discussed or investment, financial, or trading advice. Qualified professionals should be consulted prior to making financial decisions.